13.1 - Weighted Least Squares

13.1 - Weighted Least SquaresThe method of ordinary least squares assumes that there is constant variance in the errors (which is called homoscedasticity). The method of weighted least squares can be used when the ordinary least squares assumption of constant variance in the errors is violated (which is called heteroscedasticity). The model under consideration is

\(\begin{equation*} \textbf{Y}=\textbf{X}\beta+\epsilon^{*}, \end{equation*}\)

where \(\epsilon^{*}\) is assumed to be (multivariate) normally distributed with mean vector 0 and nonconstant variance-covariance matrix

\(\begin{equation*} \left(\begin{array}{cccc} \sigma^{2}_{1} & 0 & \ldots & 0 \\ 0 & \sigma^{2}_{2} & \ldots & 0 \\ \vdots & \vdots & \ddots & \vdots \\ 0 & 0 & \ldots & \sigma^{2}_{n} \\ \end{array} \right) \end{equation*}\)

If we define the reciprocal of each variance, \(\sigma^{2}_{i}\), as the weight, \(w_i = 1/\sigma^{2}_{i}\), then let matrix W be a diagonal matrix containing these weights:

\(\begin{equation*}\textbf{W}=\left( \begin{array}{cccc} w_{1} & 0 & \ldots & 0 \\ 0& w_{2} & \ldots & 0 \\ \vdots & \vdots & \ddots & \vdots \\ 0& 0 & \ldots & w_{n} \\ \end{array} \right) \end{equation*}\)

The weighted least squares estimate is then

\(\begin{align*} \hat{\beta}_{WLS}&=\arg\min_{\beta}\sum_{i=1}^{n}\epsilon_{i}^{*2}\\ &=(\textbf{X}^{T}\textbf{W}\textbf{X})^{-1}\textbf{X}^{T}\textbf{W}\textbf{Y} \end{align*}\)

With this setting, we can make a few observations:

- Since each weight is inversely proportional to the error variance, it reflects the information in that observation. So, an observation with a small error variance has a large weight since it contains relatively more information than an observation with a large error variance (small weight).

- The weights have to be known (or more usually estimated) up to a proportionality constant.

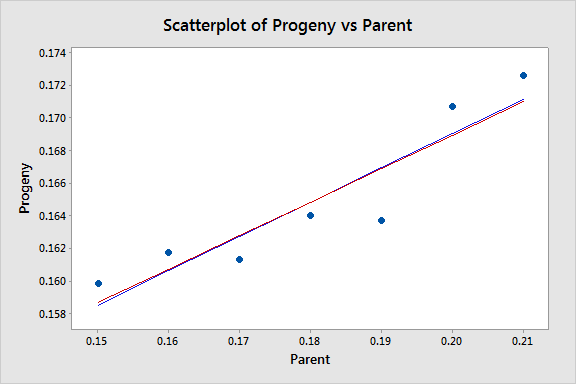

To illustrate, consider the famous 1877 Galton data set, consisting of 7 measurements each of X = Parent (pea diameter in inches of parent plant) and Y = Progeny (average pea diameter in inches of up to 10 plants grown from seeds of the parent plant). Also included in the dataset are standard deviations, SD, of the offspring peas grown from each parent. These standard deviations reflect the information in the response Y values (remember these are averages) and so in estimating a regression model we should downweight the observations with a large standard deviation and upweight the observations with a small standard deviation. In other words, we should use weighted least squares with weights equal to \(1/SD^{2}\). The resulting fitted equation from Minitab for this model is:

Progeny = 0.12796 + 0.2048 Parent

Compare this with the fitted equation for the ordinary least squares model:

Progeny = 0.12703 + 0.2100 Parent

The equations aren't very different but we can gain some intuition into the effects of using weighted least squares by looking at a scatterplot of the data with the two regression lines superimposed:

The black line represents the OLS fit, while the red line represents the WLS fit. The standard deviations tend to increase as the value of Parent increases, so the weights tend to decrease as the value of Parent increases. Thus, on the left of the graph where the observations are up-weighted the red fitted line is pulled slightly closer to the data points, whereas on the right of the graph where the observations are down-weighted the red fitted line is slightly further from the data points.

For this example, the weights were known. There are other circumstances where the weights are known:

- If the i-th response is an average of \(n_i\) equally variable observations, then \(Var\left(y_i \right)\) = \(\sigma^2/n_i\) and \(w_i\) = \(n_i\).

- If the i-th response is a total of \(n_i\) observations, then \(Var\left(y_i \right)\) = \(n_i\sigma^2\) and \(w_i\) =1/ \(n_i\).

- If variance is proportional to some predictor \(x_i\), then \(Var\left(y_i \right)\) = \(x_i\sigma^2\) and \(w_i\) =1/ \(x_i\).

In practice, for other types of datasets, the structure of W is usually unknown, so we have to perform an ordinary least squares (OLS) regression first. Provided the regression function is appropriate, the i-th squared residual from the OLS fit is an estimate of \(\sigma_i^2\) and the i-th absolute residual is an estimate of \(\sigma_i\) (which tends to be a more useful estimator in the presence of outliers). The residuals are much too variable to be used directly in estimating the weights, \(w_i,\) so instead we use either the squared residuals to estimate a variance function or the absolute residuals to estimate a standard deviation function. We then use this variance or standard deviation function to estimate the weights.

Some possible variance and standard deviation function estimates include:

- If a residual plot against a predictor exhibits a megaphone shape, then regress the absolute values of the residuals against that predictor. The resulting fitted values of this regression are estimates of \(\sigma_{i}\). (And remember \(w_i = 1/\sigma^{2}_{i}\)).

- If a residual plot against the fitted values exhibits a megaphone shape, then regress the absolute values of the residuals against the fitted values. The resulting fitted values of this regression are estimates of \(\sigma_{i}\).

- If a residual plot of the squared residuals against a predictor exhibits an upward trend, then regress the squared residuals against that predictor. The resulting fitted values of this regression are estimates of \(\sigma_{i}^2\).

- If a residual plot of the squared residuals against the fitted values exhibits an upward trend, then regress the squared residuals against the fitted values. The resulting fitted values of this regression are estimates of \(\sigma_{i}^2\).

After using one of these methods to estimate the weights, \(w_i\), we then use these weights in estimating a weighted least squares regression model. We consider some examples of this approach in the next section.

Some key points regarding weighted least squares are:

- The difficulty, in practice, is determining estimates of the error variances (or standard deviations).

- Weighted least squares estimates of the coefficients will usually be nearly the same as the "ordinary" unweighted estimates. In cases where they differ substantially, the procedure can be iterated until estimated coefficients stabilize (often in no more than one or two iterations); this is called iteratively reweighted least squares.

- In some cases, the values of the weights may be based on theory or prior research.

- In designed experiments with large numbers of replicates, weights can be estimated directly from sample variances of the response variable at each combination of predictor variables.

- The use of weights will (legitimately) impact the widths of statistical intervals.

13.1.1 - Weighted Least Squares Examples

13.1.1 - Weighted Least Squares ExamplesExample 13-1: Computer-Assisted Learning Dataset

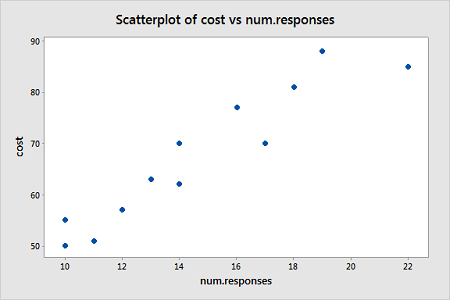

The Computer-Assisted Learning New data was collected from a study of computer-assisted learning by n = 12 students.

| i | Responses | Cost |

|---|---|---|

| 1 | 16 | 77 |

| 2 | 14 | 70 |

| 3 | 22 | 85 |

| 4 | 10 | 50 |

| 5 | 14 | 62 |

| 6 | 17 | 70 |

| 7 | 10 | 55 |

| 8 | 13 | 63 |

| 9 | 19 | 88 |

| 10 | 12 | 57 |

| 11 | 18 | 81 |

| 12 | 11 | 51 |

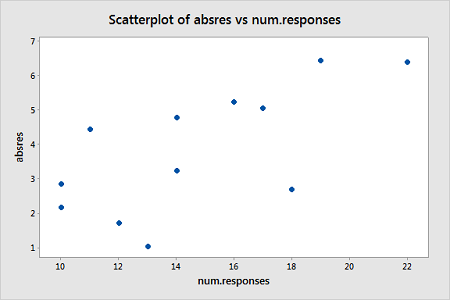

The response is the cost of the computer time (Y) and the predictor is the total number of responses in completing a lesson (X). A scatterplot of the data is given below.

From this scatterplot, a simple linear regression seems appropriate for explaining this relationship.

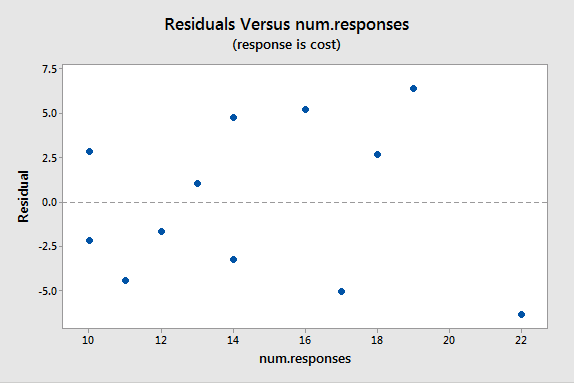

First, an ordinary least squares line is fit to this data. Below is the summary of the simple linear regression fit for this data

Model Summary

| S | R-sq | R-sq(adj) | R-sq(pred) |

|---|---|---|---|

| 4.59830 | 88.91% | 87.80% | 81.27% |

Coefficients

| Term | Coef | SE Coef | T-Value | P-Value | VIF |

|---|---|---|---|---|---|

| Constant | 19.47 | 5.52 | 3.53 | 0.005 | |

| num.responses | 3.269 | 0.365 | 8.95 | 0.000 | 1.00 |

Regression Equation

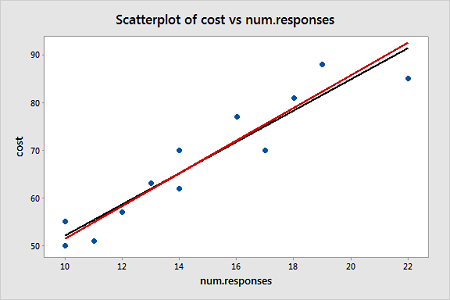

cost = 19.47 + 3.269 num.responses

A plot of the residuals versus the predictor values indicates possible nonconstant variance since there is a very slight "megaphone" pattern:

We will turn to weighted least squares to address this possibility. The weights we will use will be based on regressing the absolute residuals versus the predictor. In Minitab, we can use the Storage button in the Regression Dialog to store the residuals. Then we can use Calc > Calculator to calculate the absolute residuals. A plot of the absolute residuals versus the predictor values is as follows:

The weights we will use will be based on regressing the absolute residuals versus the predictor. Specifically, we will fit this model, use the Storage button to store the fitted values, and then use Calc > Calculator to define the weights as 1 over the squared fitted values. Then we fit a weighted least squares regression model by fitting a linear regression model in the usual way but clicking "Options" in the Regression Dialog and selecting the just-created weights as "Weights."

The summary of this weighted least squares fit is as follows:

Model Summary

| S | R-sq | R-sq(adj) | R-sq(pred) |

|---|---|---|---|

| 1.15935 | 89.51% | 88.46% | 83.87% |

Coefficients

| Term | Coef | SE Coef | T-Value | P-Value | VIF |

|---|---|---|---|---|---|

| Constant | 17.30 | 4.83 | 3.58 | 0.005 | |

| num.responses | 3.421 | 0.370 | 9.24 | 0.000 | 1.00 |

Notice that the regression estimates have not changed much from the ordinary least squares method. The following plot shows both the OLS fitted line (black) and WLS fitted line (red) overlaid on the same scatterplot.

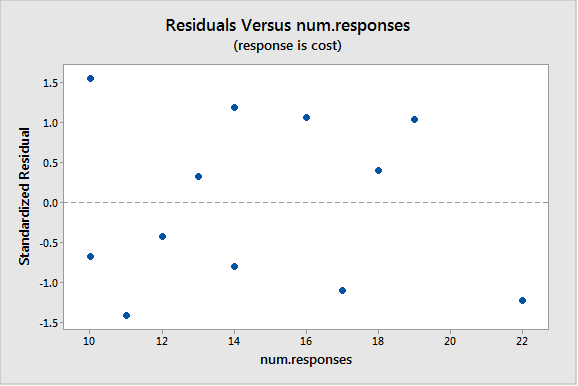

A plot of the studentized residuals (remember Minitab calls these "standardized" residuals) versus the predictor values when using the weighted least squares method shows how we have corrected for the megaphone shape since the studentized residuals appear to be more randomly scattered about 0:

With weighted least squares, it is crucial that we use studentized residuals to evaluate the aptness of the model since these take into account the weights that are used to model the changing variance. The usual residuals don't do this and will maintain the same non-constant variance pattern no matter what weights have been used in the analysis.

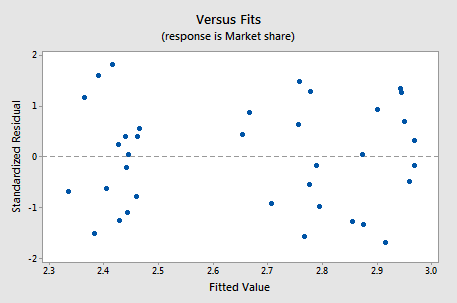

Example 13-2: Market Share Data

Here we have market share data for n = 36 consecutive months (Market Share data). Let Y = market share of the product; \(X_1\) = price; \(X_2\) = 1 if the discount promotion is in effect and 0 otherwise; \(X_2\)\(X_3\) = 1 if both discount and package promotions in effect and 0 otherwise. The regression results below are for a useful model in this situation:

Coefficients

| Term | Coef | SE Coef | T-Value | P-Value | VIF |

|---|---|---|---|---|---|

| Constant | 3.196 | 0.356 | 8.97 | 0.000 | |

| Price | -0.334 | 0.152 | -2.19 | 0.036 | 1.01 |

| Discount | 0.3081 | 0.0641 | 4.80 | 0.000 | 1.68 |

| DiscountPromotion | 0.1762 | 0.0660 | 2.67 | 0.012 | 1.69 |

This model represents three different scenarios:

- Months in which there was no discount (and either a package promotion or not): X2 = 0 (and X3 = 0 or 1);

- Months in which there was a discount but no package promotion: X2 = 1 and X3 = 0;

- Months in which there was both a discount and a package promotion: X2 = 1 and X3 = 1.

So, it is fine for this model to break the hierarchy if there is no significant difference between the months in which there was no discount and no package promotion and months in which there was no discount but there was a package promotion.

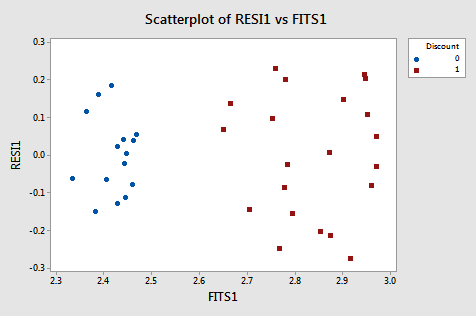

A residual plot suggests nonconstant variance related to the value of \(X_2\):

From this plot, it is apparent that the values coded as 0 have a smaller variance than the values coded as 1. The residual variances for the two separate groups defined by the discount pricing variable are:

| Discount | N | StDev | Variance | 95% CI for StDevs |

|---|---|---|---|---|

| 0 | 15 | 0.103 | 0.011 | (0.077, 0.158) |

| 1 | 21 | 0.164 | 0.027 | (0.136, 0.217) |

Because of this nonconstant variance, we will perform a weighted least squares analysis. For the weights, we use \(w_i=1 / \hat{\sigma}_i^2\) for i = 1, 2 (in Minitab use Calc > Calculator and define "weight" as ‘Discount'/0.027 + (1-‘Discount')/0.011 . The weighted least squares analysis (set the just-defined "weight" variable as "weights" under Options in the Regression dialog) is as follows:

Analysis of Variance

| Source | DF | Adj SS | Adj MS | F-Value | P-Value |

|---|---|---|---|---|---|

| Regression | 3 | 96.109 | 32.036 | 30.84 | 0.000 |

| Price | 1 | 4.688 | 4.688 | 4.51 | 0.041 |

| Discount | 1 | 23.039 | 23.039 | 22.18 | 0.000 |

| DiscountPromotion | 1 | 5.634 | 5.634 | 5.42 | 0.026 |

| Error | 32 | 33.246 | 1.039 | ||

| Total | 35 | 129.354 |

Coefficients

| Term | Coef | SE Coef | T-Value | P-Value | VIF |

|---|---|---|---|---|---|

| Constant | 3.175 | 0.357 | 8.90 | 0.000 | |

| Price | -0.325 | 0.153 | -2.12 | 0.041 | 1.01 |

| Discount | 0.3083 | 0.0655 | 4.71 | 0.000 | 2.04 |

| DiscountPromotion | 0.1759 | 0.0755 | 2.33 | 0.026 | 2.05 |

An important note is that Minitab’s ANOVA will be in terms of the weighted SS. When doing a weighted least squares analysis, you should note how different the SS values of the weighted case are from the SS values for the unweighted case.

Also, note how the regression coefficients of the weighted case are not much different from those in the unweighted case. Thus, there may not be much of an obvious benefit to using the weighted analysis (although intervals are going to be more reflective of the data).

If you proceed with a weighted least squares analysis, you should check a plot of the residuals again. Remember to use the studentized residuals when doing so! For this example, the plot of studentized residuals after doing a weighted least squares analysis is given below and the residuals look okay (remember Minitab calls these standardized residuals).

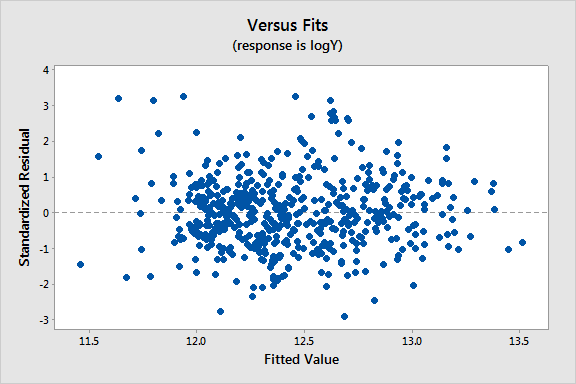

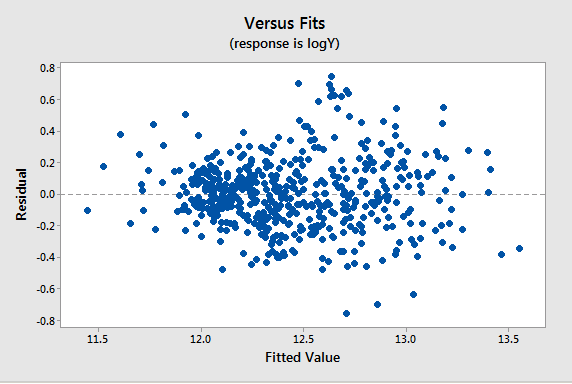

Example 13-3: Home Price Dataset

The Home Price data set has the following variables:

Y = sale price of a home

\(X_1\) = square footage of the home

\(X_2\) = square footage of the lot

Since all the variables are highly skewed we first transform each variable to its natural logarithm. Then when we perform a regression analysis and look at a plot of the residuals versus the fitted values (see below), we note a slight “megaphone” or “conic” shape of the residuals.

| Term | Coef | SE Coeff | T-Value | P-Value | VIF |

|---|---|---|---|---|---|

| Constant | 1.964 | 0.313 | 6.28 | 0.000 | |

| logX1 | 1.2198 | 0.0340 | 35.87 | 0.000 | 1.05 |

| logX2 | 0.1103 | 0.0241 | 4.57 | 0.000 | 1.05 |

We interpret this plot as having a mild pattern of nonconstant variance in which the amount of variation is related to the size of the mean (which are the fits).

So, we use the following procedure to determine appropriate weights:

- Store the residuals and the fitted values from the ordinary least squares (OLS) regression.

- Calculate the absolute values of the OLS residuals.

- Regress the absolute values of the OLS residuals versus the OLS fitted values and store the fitted values from this regression. These fitted values are estimates of the error standard deviations.

- Calculate weights equal to \(1/fits^{2}\), where "fits" are the fitted values from the regression in the last step.

We then refit the original regression model but use these weights this time in a weighted least squares (WLS) regression.

Results and a residual plot for this WLS model:

| Term | Coef | SE Coeff | T-Value | P-Value | VIF |

|---|---|---|---|---|---|

| Constant | 2.377 | 0.284 | 8.38 | 0.000 | |

| logX1 | 1.2014 | 0.0336 | 35.72 | 0.000 | 1.08 |

| logX2 | 0.0831 | 0.0217 | 3.83 | 0.000 | 1.08 |